filmov

tv

how to perform garch stata13

0:07:06

Stata - How to Estimate (G)ARCH Models

0:14:06

Estimating a GARCH model in Stata

0:14:12

(EViews10): How to Perform GARCH Diagnostics #garch #diagnostics #garchdiagnostics #archdiagnostics

0:10:22

Stata Tutorial: Threshold ARCH Model

0:14:25

(EViews10): How to Estimate Standard GARCH Models #garch #arch #volatility #clustering #archlm

0:09:12

(Stata13): How to Perform Johansen Cointegration Test #var #vecm #Johansen #cointegration

0:07:07

Basics of GARCH Modeling #garch #garchmodeling #financialeconometrics #garch-m #tgarch #egarch

1:09:01

Basics of GARCH Modeling - Time Series Modeling Technique

0:14:54

E Garch 1 1 (Part 9)

0:07:52

(EViews10): How to Estimate GARCH-in-Mean Models #garchmodels #garchm #tgarch #volatility #egarch

0:07:45

(EViews10): How to Estimate Exponential GARCH Models #garchm #tgarch #egarch #igarch #cgarch #arch

0:24:48

ARCH GARCH Modeling through STATA

0:05:51

(EViews10): ARCH vs. GARCH Models (Estimations) #garch #arch #parsimony #volatility

0:22:16

M-34. GARCH model

0:10:45

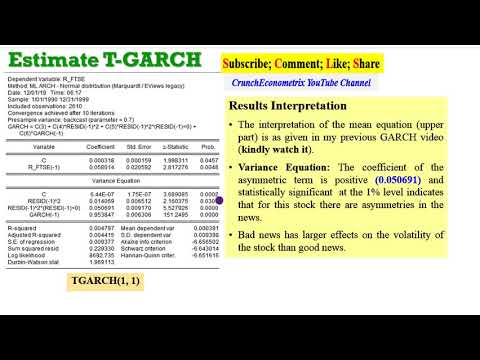

(EViews10): How to Estimate Threshold GARCH (GJR-GARCH) #garchm #tgarch #egarch #gjr-garch

0:13:27

Tesis & Econometría: Regresión lineal ENAHO en STATA 13

0:01:49

GARCH final

0:11:03

ARCH vs GARCH (The Background) #garch #arch #clustering #volatility #mgarch #tgarch #egarch #igarch

0:02:59

Interpretation Linear probability model

0:13:45

Tesis & Econometría: Modelos Vectores Auto Regresivos VAR y SVAR en STATA 13

0:17:54

Tesis & Econometría: Series de Tiempo en STATA 13

0:02:06

Econometrics workshop Part 1

0:00:38

Inflation Volatility

0:23:55

Pemodelan VAR-GARCH pada data Inflasi, IHK, dan Nilai Tukar Ekspor Impor Provinsi Sulawesi Tengah

Вперёд

visit shbcf.ru

0:07:06

0:07:06

0:14:06

0:14:06

0:14:12

0:14:12

0:10:22

0:10:22

0:14:25

0:14:25

0:09:12

0:09:12

0:07:07

0:07:07

1:09:01

1:09:01

0:14:54

0:14:54

0:07:52

0:07:52

0:07:45

0:07:45

0:24:48

0:24:48

0:05:51

0:05:51

0:22:16

0:22:16

0:10:45

0:10:45

0:13:27

0:13:27

0:01:49

0:01:49

0:11:03

0:11:03

0:02:59

0:02:59

0:13:45

0:13:45

0:17:54

0:17:54

0:02:06

0:02:06

0:00:38

0:00:38

0:23:55

0:23:55